Broken by Design: Why Merchant Settlement Still Feels Broken

For most consumers, payments already feel instant.

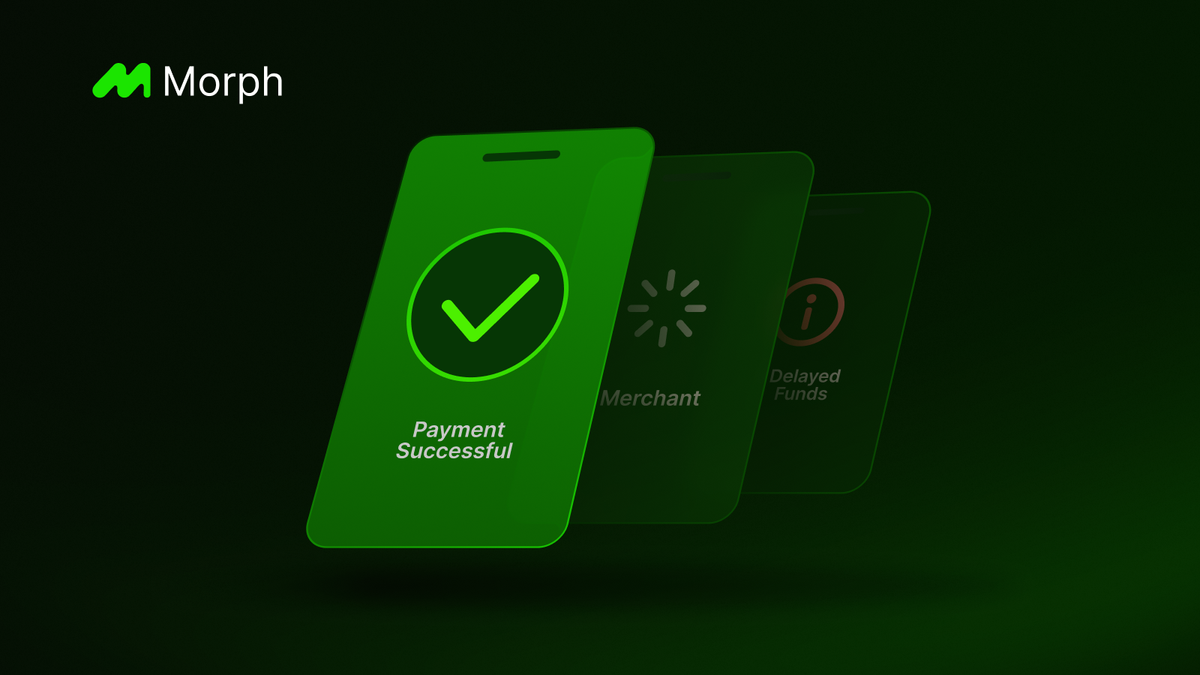

You tap a card, click checkout, or confirm a purchase in an app, and the transaction appears complete. The experience is fast, familiar, and increasingly invisible.

For merchants, it feels very different.

Behind the checkout confirmation, funds may still take days to settle. Reconciliation may require multiple systems. Treasury teams may still be waiting for money that customers assume has already arrived.

The issue is not that checkout has failed to improve. It is that settlement has improved more slowly than the user experience layered on top of it. Merchant settlement still feels broken because the rails behind it were not designed for the speed, flexibility, and operating model modern businesses now expect.

The Customer Experience Moved Faster Than the Rails

The front end of payments has evolved quickly.

User interfaces improved. Mobile payments became normal. Checkout flows became smoother. Fraud tools became more sophisticated. More of the payment process moved into the background.

What did not improve at the same pace was what happens after the customer pays.

Authorization may happen in seconds. Final settlement often does not.

That creates a structural gap between what the user sees and what the business experiences. To the customer, the transaction is done. To the merchant, the money may still be moving through processors, acquirers, card networks, banks, and settlement schedules before it is actually usable.

The experience feels modern. The rails behind it often do not.

Why This Still Hurts Merchants

Settlement delay is not just a back-office inconvenience. It has real operating consequences.

When funds take longer to settle, merchants feel it in several ways:

- cash flow becomes harder to predict

- reconciliation takes more effort

- treasury operations become less efficient

- working capital remains trapped in transit

- cross-border and multi-currency flows become more expensive to manage

For large businesses, that drag compounds across high transaction volume. For smaller businesses, it can be even more painful, because access to funds directly affects day-to-day operations.

The problem is not only that merchants wait. It is that they often absorb that delay as a hidden cost of doing business.

Settlement Friction Is Still Baked Into the System

A lot of merchant infrastructure still reflects older assumptions about how money should move.

Those assumptions include:

- that settlement can happen later than the user action

- that intermediaries are unavoidable

- that business-hour coordination is normal

- that delays are acceptable if checkout remains smooth

That may have made sense in earlier financial systems. It makes less sense in a world where digital businesses operate continuously, customers expect immediacy, and money movement increasingly defines product quality.

The merchant settlement experience still depends on too many layers that were designed around institutional convenience rather than operational efficiency for the business receiving funds.

That is why the problem persists. It is not a bug at the edge. It is built into the architecture.

What Better Settlement Changes

When settlement improves, a lot more than speed improves with it.

Faster, cleaner settlement can mean:

- quicker access to revenue

- lower reconciliation burden

- more efficient treasury movement

- better liquidity planning

- simpler cross-border operations

- less working capital sitting in motion instead of being used

For merchants, that changes the economics of payment operations.

The value is not only in getting paid faster. It is in making the overall payment system easier to run, easier to trust, and easier to build around.

That matters even more as payment products expand into global commerce, real-time payouts, and stablecoin-based transaction flows.

Why Stablecoin Rails Matter Here

Stablecoin payments matter for merchants because they compress the path between payment and usable funds.

Instead of routing through multiple institutionally layered systems before settlement is final, stablecoin-based rails can make movement and settlement more direct, more transparent, and more available across time zones and operating hours.

That does not eliminate every operational challenge, but it changes the structure of the flow.

With better rails, merchants can move closer to a system where:

- settlement happens faster

- funds are visible sooner

- payment infrastructure is easier to integrate

- global transactions are less dependent on legacy cutoffs and intermediaries

That is why stablecoins are increasingly relevant beyond crypto-native use cases. For merchants, the upside is operational.

How Morph Aims to Support This Shift

Morph is built around a simple idea: payment infrastructure should be designed for real movement of value, not just transaction throughput.

That matters in merchant settlement because merchants need more than successful checkout. They need timely, predictable access to funds and a settlement layer that supports real business flows at scale.

Morph is positioned to support that in several ways.

Faster Settlement for Real Payment Flows

Morph is designed for high-volume payment activity, with fast block times and infrastructure built around movement of value rather than purely speculative activity.

For merchants and payment applications, that creates an environment where settlement can feel closer to the pace of the user interaction itself.

Stablecoin-Native Infrastructure

Merchants do not need more complexity in how value settles. They need reliable dollar-denominated and other stable settlement assets they can build around.

Morph’s stablecoin integrations help make that possible, giving builders and payment products access to assets designed for real movement of value rather than fragmented or improvised payment flows.

Better Economics for Builders and Operators

Merchant settlement is not solved by speed alone. It also depends on cost structure, reliability, and ease of integration.

Morph’s broader design - low-cost transfers, payment-oriented infrastructure, and a growing ecosystem of stablecoin, wallet, bridge, and payment partners - helps reduce the friction businesses face when building or operating merchant-facing payment products.

A Foundation for More Modern Commerce

As payments become more programmable, more global, and more integrated into software, merchants need rails that match that operating model.

Morph is building toward a world where the gap between “customer paid” and “merchant can use the funds” becomes much smaller than it is today.

That is a meaningful shift in how commerce works.

The Bigger Point

Merchant settlement is one of those problems that hides behind good interface design.

Customers rarely think about it. Businesses have to.

That is why it matters so much.

The market has spent years improving what paying looks like. The next stage is improving what getting settled actually feels like for the business on the other side.

That is a rails problem. And it is increasingly one that better infrastructure can solve.

Conclusion

Merchant settlement still feels broken because the visible part of payments improved faster than the system beneath it.

The result is a familiar gap: customers pay instantly, while merchants wait for settlement, manage delayed funds, and absorb the cost of operating across outdated rails.

That gap is no longer easy to defend.

As commerce becomes more digital, more global, and more dependent on efficient movement of value, settlement becomes too important to remain slow, opaque, or institutionally fragmented.

The better the rails get, the smaller that gap becomes.

And for merchants, that may be one of the most important payment shifts still ahead.