Broken by Design: Why Remittances Still Cost Too Much

For millions of people around the world, remittances are not an edge case. They are essential infrastructure.

They pay rent. They cover groceries. They support parents, children, and entire households across borders. In many markets, remittance flows are not just personal transfers. They are a meaningful part of the broader economy. And yet, sending money home is still far more expensive, slower, and more fragmented than it should be.

This is often treated as an unfortunate reality of global finance. It should be treated as a design failure.

The problem is not demand. The problem is the rails.

Remittances Are Still Built on Too Many Intermediaries

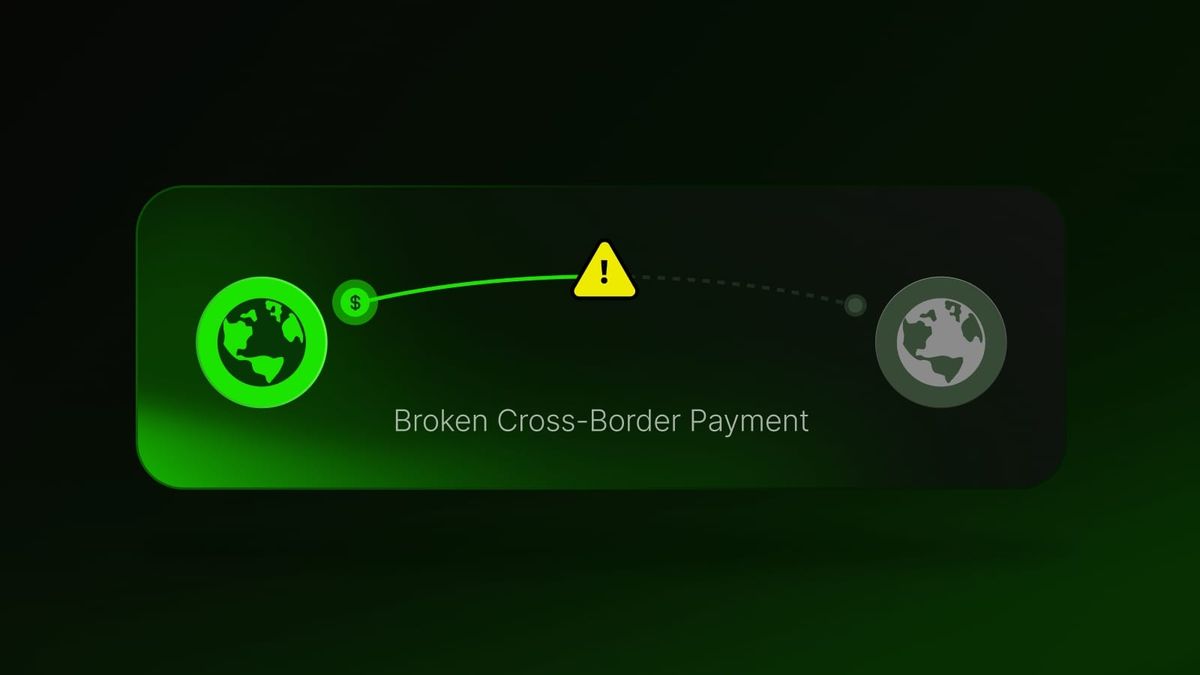

A typical cross-border transfer still moves through a chain of institutions before it reaches the recipient.

Banks. Correspondent banks. Payment processors. FX intermediaries. Local payout networks. Compliance layers. Settlement partners.

Each layer has its own rules, operating windows, fees, and dependencies. Each layer adds friction. Each layer introduces another place for value to be delayed, reduced, or obscured.

By the time the transfer arrives, the sender has often paid more than expected, the recipient has waited longer than they should have, and neither side has much visibility into where the time or cost was absorbed.

This is not a user experience issue at the edge. It is a structural issue at the core.

The Hidden Cost of Legacy Remittance Rails

Remittance pain is usually described in terms of fees, but the problem runs deeper than the visible charge on the screen.

The cost shows up in multiple places at once:

- transfer fees charged upfront

- FX spreads buried in the conversion process

- delayed settlement across intermediaries

- banking cutoffs and non-business-hour slowdowns

- fragmented payout options depending on the destination market

What looks like a simple transfer is often a layered process where cost compounds before value reaches the end user.

For people sending money home regularly, these costs are not abstract. They reduce how much actually arrives.

For businesses facilitating payouts, they create operational drag, reconciliation friction, and weaker unit economics.

Speed Still Matters More Than the Industry Admits

A remittance is not complete when the sender clicks send. It is complete when the recipient can actually use the funds.

That sounds obvious, but much of the legacy financial system is still optimized around institutional process, not recipient experience.

Settlement delays persist because the system still assumes money should move according to banking windows, cutoffs, and manual coordination between institutions. The world, meanwhile, has moved on. People expect digital systems to work in real time. Their financial lives do not stop at weekends, holidays, or geography.

Remittances are one of the clearest examples of this mismatch.

The demand is immediate. The infrastructure often is not.

Why Stablecoins Change the Equation

Stablecoins matter in remittances because they simplify the path money takes from sender to recipient.

Instead of relying on multiple institutional layers to coordinate value transfer, stablecoins make it possible to move a digital dollar or local-currency-pegged asset directly across blockchain infrastructure with faster finality and fewer intermediaries in the middle.

That changes the economics of the flow.

A better remittance path can mean:

- faster settlement

- clearer movement of funds

- reduced dependence on correspondent banking layers

- lower friction across borders

- simpler treasury management for payout providers

- more of the value arriving at the endpoint

The improvement is not just technical. It is practical.

When the rails improve, the user feels it in cost, speed, and reliability.

But Stablecoins Alone Are Not the Full Solution

A stablecoin by itself does not fix remittances.

The full system still needs:

- accessible onramps and offramps

- predictable settlement infrastructure

- sufficient liquidity

- support for local currency corridors

- integration into wallets, payment apps, and business workflows

- compliance and operational reliability at scale

That is why the next phase of remittance innovation is not just about issuing more assets. It is about building the settlement and liquidity layer around them.

If remittances are going to improve meaningfully, the infrastructure underneath them has to be purpose-built for high-frequency, cross-border movement of value.

How Morph Aims to Support This Shift

Morph is built around a simple belief: global payments need better settlement rails.

That matters in remittances because remittance flows are highly sensitive to delay, cost, and fragmentation. The faster value settles and the fewer layers it passes through, the better the economics become for both providers and recipients.

Morph is designed to support that shift in a few important ways.

Fast, Payment-Oriented Settlement

Morph is built for high-volume payment flows, with fast block times and infrastructure designed to support real movement of value rather than speculative throughput metrics.

For remittance providers and payment applications, that means a better settlement environment for flows that need to move quickly and predictably.

Stablecoin-Native Design

Stablecoins sit at the center of real-world payment activity, especially in cross-border use cases. Morph’s infrastructure is designed to support stablecoin settlement directly, helping reduce the operational complexity that often appears when systems are not built around payment assets from the start.

Lower Friction for Moving Value Onchain

Cross-border payment systems increasingly need to pull liquidity from multiple ecosystems and route it efficiently. Morph’s growing interoperability layer and stablecoin integrations are part of making that movement easier, so remittance-related flows do not get stuck behind fragmented access points.

A Builder Environment for Payment Products

Remittances are not solved by one app or one asset. They are solved by an ecosystem of providers, rails, onramps, settlement layers, and payout experiences working together.

Morph’s broader strategy, including the Payment Accelerator, is aimed at helping teams build those kinds of real-world payment products onchain.

That includes the kind of infrastructure remittance companies, stablecoin payment providers, and fintech platforms need if they are going to operate across borders more efficiently.

The Real Opportunity

Remittances are one of the clearest proof points for why payment infrastructure still needs to improve.

The problem is widely understood. The user demand is already there. The inefficiencies are obvious. The only thing that has been missing is a better way to move value across borders without layering cost and delay into every step.

That is what makes this category so important.

Remittances are not just a use case for better rails. They are one of the strongest arguments for why those rails need to exist in the first place.

Conclusion

Sending money home should not still feel this hard.

It should not take this long. It should not cost this much. It should not require so many institutions to coordinate behind the scenes just for value to arrive where it is needed.

Remittances remain expensive because the system they rely on was built around intermediaries, delays, and geographic fragmentation. That is not an inevitable condition of moving money. It is a product of infrastructure design.

Stablecoins offer a better starting point. Better settlement layers make that starting point more usable. And as more payment systems are rebuilt around speed, transparency, and lower-cost global transfer, remittances may become one of the first categories where users feel the difference clearly.

That is the opportunity.

And it starts with better rails.